Coronavirus, code named COVID-19 which stands for Coronavirus Disease 2019, has become a household name in the entire world, everyone including kids know how dangerous it is and its impact on a human body.

I won’t dive deep into COVID-19 details rather we will gauge it’s impact on global economy and how, possibly, it could be an opportunity to invest in stocks, ETFs and Mutual funds?

Not sure if you follow stock market but if you don’t then you are definitely at a receiving end in today’s time. Everyone from a CEO, Engineer, Sports person or a Lay man knows how to earn money, but there are only few who know how to manage money. When I said manage money that means we have clear understanding of our wants and needs, where when and how we need to spend or invest. Most of the time families live paycheck to paycheck, there is a famous saying in North America “We are just one paycheck away from poverty.”, so spend and manage wisely my friends.

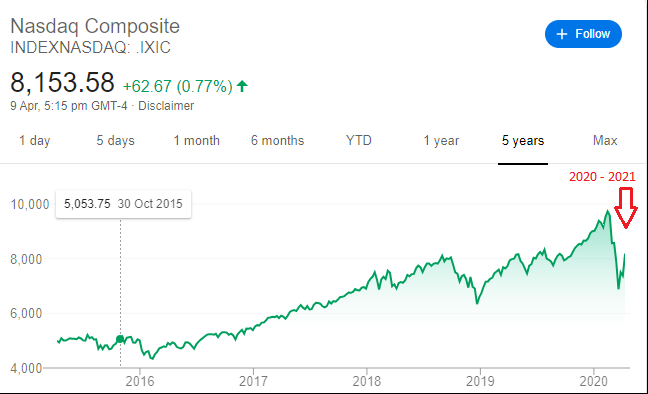

Below is screenshot of current stock market indexes of US and Canada:

US – NASDAQ

US – Dow Jones

CANADIAN – S&P/TSX Index

Look at the line graphs above, do they make any sense? I want you to look more closely when the line graph goes downwards. There are blocks of time when there was a deep dive of stock market, one around 2008-2009 time period, and the other one is around 2020 – 2021. These are the times when stock markets all around the word were badly impacted due to one reason or the other.

During 2008-2009 time period it was famous subprime mortgage crisis in US that triggered recession. In 2020-2021 it was due to COVID-19 aka (also known as) Coronavirus Disease 2019. During these tough times mostly every normal life was impacted, it was clearly visible from the stock market trends around that time.

During COVID-19 timeframe, a strict lockdown was declared in many countries, that lockdown was more like a curfew, it went for many months. People were mandatorily advised to stay inside their houses. Businesses, jobs, every life & industrial sector were impacted, hence it resulted in the stock market crash. People who were close to retirement lost lots and lots of their hard earned money, especially those who didn’t have enough appetite to hold on to their stocks or mutual for some more time knowing the market mainly bounces back after a major crash.

Anyway, above are some facts and history about stock market indexes, and their performance year over year.

May be I will start from my story first before we get into too much details about investing and all.

I was never into stocks or investment till 2006, I was happy working and spending in Canada 🙂 . Around end of year 2006 someone introduced me to the concept of RRSP and it’s benefits. RRSP stands for Registered Retired Savings Plan, and how as a Canadian I can make contribution to it which will act as tax deferral. More about RRSP can be found here link. When I heard about tax benefits, it got my attention.

The agent who told me about RRSP then went to the next step about how to contribute to RRSP, remember it was year 2006 Google was still making its hold on the world of internet. To put it simple, I didn’t do much Googling to understand fully about RRSP 🙁 , my bad but hey if we aren’t making mistakes then we aren’t learning 🙂 . But it wasn’t a mistake at all, but yes lack of knowledge was definitely a mistake.

The agent then told me about the concepts of mutual funds, and how I could invest my RRSP dollars into mutual funds. He showed me a great picture of the best of the best AGF funds, I also learnt a bit about the world of Mutual Funds from him. The agent showed me all the good graphs of few funds that were performing really well, after an hour so I was convinced that I should put my RRSP money into AGF Mutual funds, and so I did. Filed my taxes in year 2007, and was happy to see CRA (Canada Revenue Agency) returned some of my money back due to my RRSP contributions, that was some good feeling to be very frank 🙂

So far life was going on well, we were done with the RRSP contribution for year 2006, and now life was back to normal. Once in a while I used to look at my funds which were performing ok ok, but not to my high expectations that were set by the agent, but no complains so far.

Now we entered into year 2008, who will forget The Great Recession—sometimes referred to as the 2008 Recession—in the United States and Western Europe has been linked to the so-called “subprime mortgage crisis.”. You can read more about 2008 recession here link.

Looking at above stock market index graphs, you will get fairly good idea how badly stock market was hit. The indexes were down almost by 30-40%, and trust me that’s a huge dip. The economies lost billion to trillion of dollars during these recessions.

What I did during the recession of 2008?

The moment I noticed my hard earned money is losing its value due to the fall of stock market, from that day I realized I need to educate myself first before even investing a single penny as mutual funds could be risky too 🙁 . The only good thing I did during recession that I didn’t sell my mutual funds, I left them as it is. At one point of time they were down by almost 40%, but since I didn’t need the money immediately so I left it untouched.

Then started my investing journey, as obvious the first name that I could find was none other than, you might have guessed by now, Mr. Warren Buffet. But I went one step further, I wanted to see who did Warren Buffet learn investing fundamentals from? That’s just my nature, I always go the root in terms of getting knowledge. Warren Buffet’s guru was Benjamin Graham. Warren Buffet followed Value Investing philosophy introduced by Benjamin Graham.

Below is a list of few books I started my initial investing learning from:

There are many blogs who can teach you about investing but always clear you fundamentals first before getting any further. Always avoid shortcuts in life.

- The Intelligent Investor: The Definitive Book on Value Investing Paperback New

- The Wealthy Barber

- A Beginner’s Guide to the Stock Market: Everything You Need to Start Making Money Today

Above books gave me enough knowledge to make some sense of Why, When and How about investing. After reading these books, I realized my decision to hold on to my RRSP mutual funds was the best decision. There is famous saying in investment world “Buy Low and Sell High”, that means buy the stocks or mutual funds when their value is low, and sell them when their value is high. It sounds pretty simple but trust me it’s very hard to predict when a particular stock will reach its bottom or peak, even Warren Buffet couldn’t and can’t predict that.

But one thing I was clear on based on the books I have read that I need to start investing as soon as possible, and I need to do it regularly. Accordingly, did some more study to figure out how and which funds I need to start with. Went to the TD Bank next day, as I said earlier I don’t like wasting my time and this is one of my major strength, discussed about RRSP and how can I start contributing to it via my back than going by any agent? This time I completely avoided the agent who told me to buy AGF funds. FYI: I went to the same bank where my salary gets deposited into my account bi-weekly, you should probably do the same, but I will leave that to you to make final call on that.

As I read in the wealthy barber book I need to contribute at least monthly, accordingly I started doing that. Every month I started contributing some %, let’s say it was 5% initially, of my paycheck towards RRSP. One thing I learnt from my previous RRSP contribution is that never invest a huge amount in a fund directly, try to break it down in smaller chunks/installments, that way even the fund or stock price go higher then you are not buying a lot at highest price. But real benefit of this approach comes when fund/stock price goes lower, so you will be able to purchase more units, and that’s the real key for investing, make bigger purchases when the market is down.

Also, you don’t have to put 5% of your salary, whatever you can afford may be $100 or even $10 do so. The goal is to start taking advantage of compound interest. There is famous saying by great Albert Einstein:

Compound interest is the eighth wonder of the world. He who understands it, earns it … he who doesn’t … pays it.

– Albert Einstein

As I said earlier I went to my bank, my bank rep showed me couple of good mutual funds I can pick from, so I told him I want safety and growth of my funds , who doesn’t want that the bank guy said 🙂 . So I picked a comfort growth fund of TD Bank. Now rather than waiting for my year to end so I could contribute to my RRSP contribution as a lump sum amount, I was regularly contributing to my RRSP month after month, this is called Time Value of Money, read more about it here link.

So above was all my passive investing life where money was automatically going through my salary into some good rated mutual fund. Once you set up the automatic process you are done, you don’t need to so anything else. Let the contribution continue, and give it latest good 3 – 4 years to actually see the real growth of your portfolio. So, try to meet you bank financial advisor once after 6 months to see how the selected fund is doing, and also in case any changes are required. Good bank normally offers financial advisor services for free as they are salaried employees plus they make money via the mutual fund sales, but you won’t see anything going directly from your pocket, so you are good here.

Now I will share more about my ACTIVE Investing journey below:

Although, I started investing in mutual funds but I was still lacking some knowledge of actively trading on the stock market, to buy and sells stocks. Reading books definitely give you good theory about investing and market, but until you get your hands dirty you will never get that confidence in active investing.

So how you get your hands dirty?

It’s simple, just buy a stock yourself, sounds scary? It should, and that’s the real beauty of it.

Until you face that fear you will never overcome it, it’s as simple as that. But then a thought process goes in your mind, what happens if the stock I bought goes down, I will lose all my hard earned money. Fair enough, so you want to taste stock market but without taking chance of losing your money…hmnn!

So what to do? internally you know you should invest as it’s mandatory for the long and sometimes short term growth, as everyone around is doing, but not sure how to over that jinx.

I will give you small tip to invest, when I started investing I only started with let’s say $100, It could be smaller amount also, but when I invested I told myself if this money goes to trash I will be all fine, I am not going to lose my sleep over it. That was a big trigger for me to try buying a stock.

Remember, when you actually buy a stock yourself trust me you feel really happy, it’s all together a different & good feeling. Also, the moment you invest in a stock for the first time trust me your actual learning starts then.

You will start monitoring the stock yourself more, this is called active investing. You will start reading more about the company you have bought stocks.

You will also see from news why the stock price goes up or down, and that’s a huge learning. Trust me no book can teach you this, it only comes by getting your hands dirty.

So now let’s fast forward to 2020:

Around January 2020 we heard about Corona virus, it was a big issue in Wuhan, China but it started spreading slowly in other countries too. North American markets were still not impacted due to this. By this time I had almost 10 years of investing experience, I made and lost some money during these 10 years, mainly I made money as I was following value and couch potato approach for investing.

One thing I learnt during my investing journey that keep an eye on big dip in the stock markets, and that’s the best and mostly surest time to invest. And during the COVID-19 outbreak stock market fall I was bit ahead of the curve. The lessons I learnt as part of my year 2008 losses and recovery paid big time during the 2020 stock market fall. And I was fortunate to invest when the market was hitting the biggest fall. I moved most of my RRSP money into equities between the period of March 9, 2020 to April 6, 2020.

After march 1, 2020 I started monitoring stock market on daily basis, whenever DOW Jones index fell by more than 1000 points I moved my money from secured investment into US, Canadian and International equities. In addition to that, I used my TFSA (Tax Free savings Account) account really well during this downturn. I had some good room for investment in TFSA account, and used it to the max by investing in US and Canadian Blue Chip companies when their stock was down by almost 30-40%. This is one such example of Value Investing. All of this was only possible because I got my hands dirty around 2007-2008 time frame, and after that never looked back.

Another thing I want to point out that how I had managed money to channel into my RRSP during the fall of 2020. There is a small story here, I changed my job around year 2018. I stayed in my previous company for almost 8 years, had accumulated handsome amount as my RRSP contributions under company’s group benefits plan.

In Canada when you move your job you need to move out your RRSP money from previous company’s group retirement plan to new company’s group retirement plan. Normally, most of the companies carry similar kind of mutual funds to invest in, but you have to sell your RRSP funds and need to buy them again as part of new company’s group retirement plan. When I left the job around 2018 the markets were performing really well, so going by theory of “Buy Low and Sell High” that’s was the good time to SELL my mutual funds in RRSP, but it wasn’t good time to BUY as market was around peak during that time.

But in any case I had to move my money out of my previous companies RRSP else I will lose the group benefits incentives.

Since I had good knowledge of value investing so I reached to my new company’s RRSP advisor, and asked him I don’t want to invest my RRSP money into Mutual funds at this point of time, rather I am looking for other options here. The advisor wasn’t much impressed with my thinking, and told me it doesn’t make sense to park money out of mutual funds. He said, even if you want to play it all safe then move your money into Canadian money market funds as they are less risky and more safe compared to other investment options.

But somehow I wasn’t convinced to move big chunks of my RRSP money into a fund even if it’s one of the safest fund. Credit to all my learning as part of my 2006 RRSP investment journey. I was favoring to move my money into something like GIC, and upon my will should be able to buy mutual funds whenever I wanted to. The advisor, time and again, told me this is not a good way to proceed, and warned me you won’t gain much as part of this strategy. He was right at that moment, but I was more concerned about investing big amount of money at once into a fund even if it was safest fund.

Next morning I called my advisor again, this time I told him can you give me a written guarantee that my money won’t go down if I invest in Canadian money market fund assuming it’s the safest fund? His answer was no. And that’s it, he knew by that time I have done my homework really well. Accordingly, he suggested we have a group plan called unlocked GIC, for now you move your money there and earn a small interest of around 2.3%, and whenever you want you can keep on purchasing mutual funds by taking money out of GIC, and there won’t be any charges as it’s all covered under my company’s group retirement plan. Boy o boy, this was the jack pot for me. I had all my RRSP sitting in GIC , and upon my wish I can buy any mutual fund of my choice.

Accordingly, we initiated the transaction to move my RRSP money from my previous company to new company’s group GIC plan. Basically, this was like I was getting second chance to improve on my mistakes 🙂 . The actual transfer took place around April 2019, and by that time TSX stock index was performing really well. I was one very happy man after that transaction, and I am pretty sure you know why 🙂 , go look at TSX index around 2019 April time frame.

Now I had good amount of money sitting in my GIC, and I was earning around 2.3% interest every month, which wasn’t bad at all as my money was all safe. But my main mission was to keep an eye on the stock market, specially I was waiting for the big fall so I could buy some good mutual funds.

Fortunately or unfortunately I left the money sitting in GIC, hello!! I am father of two kids so I got busy, totally forget about my investment sitting in GIC, earning only 2.1%. But as they say patience pays, same happened to me, around February 2020 I remember I had money sitting in GIC so I better do something good with that. And guess what around March 9, 2020 I noticed a big fall in the stock market, and this time I didn’t waste a single second to invest my money into right buckets. From that day on whenever I noticed a fall in the stock market I moved my funds mostly into US, Canadian and International equity markets. These were mainly mutual funds that were offered as part of my company’s group benefits, but I was the one who cherry picked few of them. So that was all about RRSP. My financial advisor reached out to me with a note, well thought and executed.

Let’s move to TFSA now:

My TFSA is all managed by myself, there was no group plan so I was on my own to search and invest. But I had somewhat enough knowledge where to invest, so accordingly I bought some good amount of Blue Chip stocks, ETFs and few mutual funds too.

This is how TSX stock market index was around March – April 2020

As part of value investing you search for those good companies, so called Blue Chip, that took a good hit on their stock price due to some unprecedented circumstances, and invest in them. Some of the stocks, Mutual funds and ETFs you can pick to invest during this economic downturn listed below:

WARNING: Please do your own research before investing in any of the stocks, ETFs and Mutual funds below.

STOCKS:

| Company | Stock Symbol |

| AIR CANADA | AC |

| CINEPLEX INC | CGX |

| FB | |

| SPIRIT AIRLINES INC | SAVE |

| TELUS CORP | T |

| TD Bank | TD |

| MICROSOFT | MSFT |

| ORACLE | ORCL |

| ATLASSIAN | TEAM |

| HILTON GRAND VACATION | HGV |

| CHOICE HOTELS | CHH |

| HYATT HOTELS | H |

| DELTA AIR LINES | DAL |

ETF: (They are bunch of stocks together, it will help to diversify your risk)

| ETF | Symbol |

| U.S. Global Jets ETF | JETS |

| iShares Core S&P U.S. Total Market Index ETF | XUU |

| BMO India Equity Index ETF | ZID |

| Vanguard High Dividend Yield | VYM |

| iShares Core High Dividend | HDV |

| Schwab US Equity Dividend | SCHD |

MUTUAL FUNDS: (Since I learnt a lot about investing so mutual funds is my last option as they charge higher MER fee as compared to an ETF)

| Mutual Fund Name | Symbol |

| TD US Blue Chip | TDB3091 |

| TD Comfort Growth Portfolio | TDB888 |

| TD Comfort Aggressive Growth | TDB889 |

This is the biggest post I have written so far hoping you will learn from my experience and the value of investing as early as you could.

List of few Recommended Books

| Book | Author |

| The Intelligent Investor | Benjamin Graham |

| The Wealthy Barber | David Chilton |

| A Beginner’s Guide to the Stock Market | Matthew R. Kratter |

| The Richest man in Babylon | George S. Clason |

Until next post take good care. Stay safe during this testing time of COVID-19

Thank you!

Well documented as always. Lots of details.

I have read the ‘Wealthy Barber’; good book. Another book I would recommend is ‘The Richest man in Babylon’. A quick read especially for young investors.

Another technique that comes in handy is DRIP – Dividend reinvestment Plan. This could be hands off, but effective.

Thank you Majo for reading the blog, and the wonderful feedback.

Yes, Dividend reinvestment Plan is a very good technique, thank you for pointing that out.

Also, we will add another section in this blog for recommended books, will add “The Richest man in Babylon” in that.

This blog has lots of valuable information about stock market and stocks varieties for beginners to learn. Its very amazing to read about your market experience. Great work 👍

Thank you Gurvir, your comments and suggestions always motivate us.